IPCC’18 says we now have 12 years 11 years to reduce emissions by 50% or face global heating above 2’C by the turn of century. IPBES reports we caused global extinction; Amazon rain forest is shrinking. We are already using most of available arable land (where arable land tally includes what is now forests generating the oxygen we breathe). The prevailing intensive agriculture is quickly depleting topsoils. So why exactly are we not doing anything about it?

With all the knowledge we have, it feels reasonable to expect that at some point, someone will hit the breaks. Especially once you realise there may not be enough seats for everyone on Elon Musk’s Mars-bound space ship. Unfortunately, unless we succeed to fundamentally reformulate our macroeconomic thinking, there is no kill-switch. Or perhaps there may be one, but we have no control on how and when it will be applied – more on this topic below.

But, you could argue, there is green energy transition and green finance to provide it with an ample supply of capital. Fishing quotas and the raising social awareness of plastic pollution. The ban on plastic straws. Surely, we are waking up to the scale of the crisis?

This may be correct, inasmuch as microeconomics are concerned. If you focus on pricing mechanisms, the question is simply how to internalise external environmental cost to fully reflect the social opportunity cost. If you can get that right, the problem is ‘solved’. Not necessarily the problem of environmental damage itself, but at least the problem of modeling it correctly (for a deeper dive and critique of this approach, check out Herman Daly ‘Beyond Growth’, 1997).

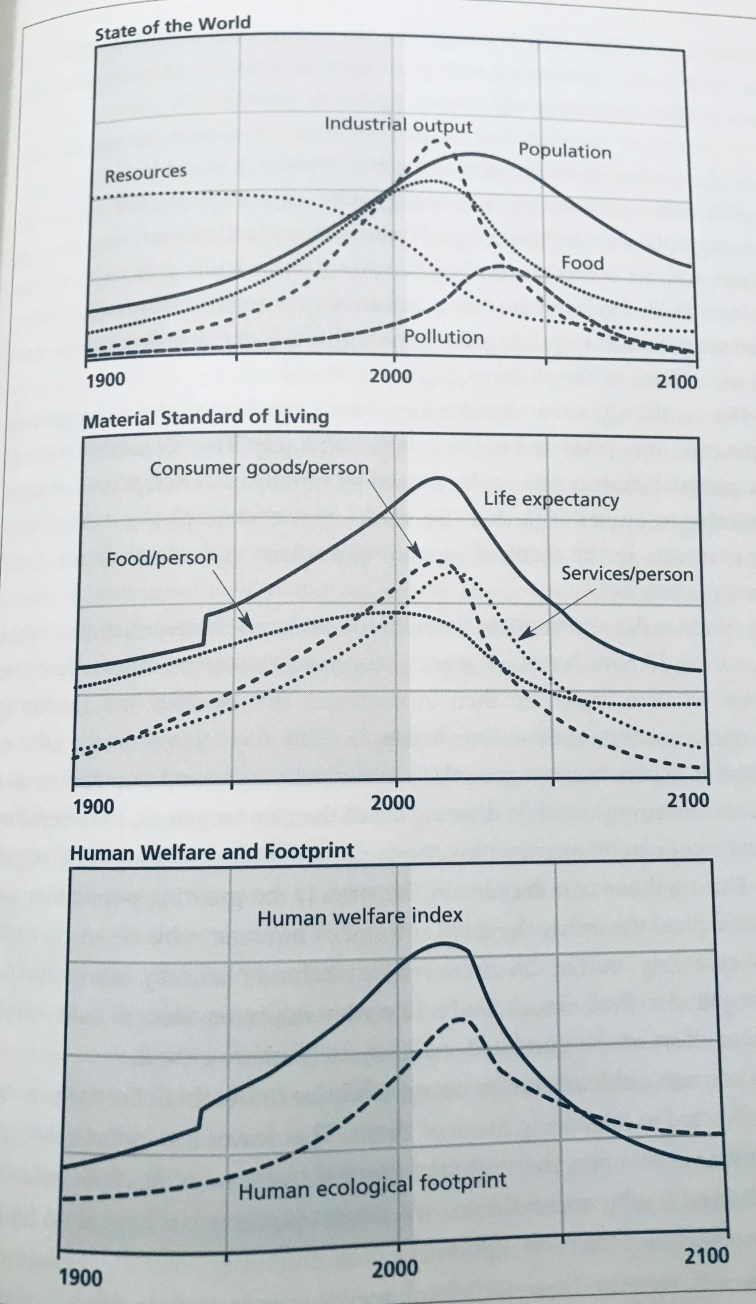

The reason why this may not work, is macroeconomics. Unlike in microeconomics, there is no concept of optimal scale of enterprise, at least not in the prevailing neoclassical economic thinking. Macroeconomics does not foresee a maximum amount of goods and services to be produced and resources to be used in the course of their production – the more the merrier, into perpetuity. Limits to Growth (LtG), a famous study published back in 1974, was the first attempt to use a computer model to present a dissenting view on growth.

LtG authors argued unchecked growth is causing depletion of resources and production waste overfilling planetary sinks (overshoot). This, in turn, will eventually cause an abrupt decline in productivity and population (collapse). Hence overshoot and collapse scenario, a nice way of saying ‘the end of the world as we know it’. Most models are showing 2050-2100 as the window when we may expect this to happen, although further iterations of LtG (there were at least two updates) have re-evaluated some of the model inputs and pushed those dates back.

The principle remains – this is what it might look like:

Pic.: LtG 2014 revision, Scenario 1: continuation of 20th century ‘business as usual’

Intuitively, this looks reasonable, given we live on a planet of a fixed diameter and with a finite, if abundant, amount of resources available. Exact timelines are up for debate, but there is less and less controversy on the overall direction of travel.

Maybe, but the fact remains that none of the three leading macroeconomic textbooks written in late 1980s (a decade after LtG!) had an entry on any of the following: environment, natural resources, pollution, depletion (see Daly p. 45, 1997). Latest Oxford Dictionary of Economics describes environment as ‘external conditions affecting human welfare and development’. Essentially, mainstream macroeconomic theory considers global economy and the environment to function separately, whilst emerging environmental economics argues a view where the economy is a subset of the environment. The fact that the latter has not really become a staple approach is a rather disturbing thought, regardless if we consider economics to be a purely descriptive, rather than a prescriptive science.

This ties back with the question of green growth financing: how can hope to have a meaningful, global sustainable investing framework, if we refuse to acknowledge the fundamental need for sustainability at macro level?

More on this soon – watch this space!